Disclaimer: If you are going to trade derivatives, be careful. Start small and learn. Always do your own research before investing. Not investment advice.

If there is interest in a deeper dive on a particular type of derivative, comment below or DM me on Twitter (@BowTiedWombat)

Introduction

This primer on derivatives will be broken into 2 parts. This post goes into the a high level overview of the various types. Part 2 walks through examples of common use cases. This post will talk about them as they are most commonly used for simplicity.

Broadly speaking there are 2 types of assets:

Cash (or physical) securities – stocks, bonds, commodities, etc.

Derivatives – swaps, forwards, futures, options etc.

Derivatives – instruments that derive their value from other assets (cash securities)

Derivatives are similar to bonds in that they have a termination date (maturity) and specified length (tenor). Derivatives have a long and a short side (or leg) to them.

The typical use cases below are examples and not recommendations.

{kind=link}

Classifications

Among derivatives there are a few distinctions:

Deliverable vs. non-deliverable (cash settled)

Listed vs. over-the-counter (OTC)

Delta One vs. Variable Delta

Deliverable

Deliverable means you must deliver the underlying security at the specified date and if certain conditions are met.

Example: If you are long an oil futures contract (CL) and hold it to maturity, you will be delivered 1,000 barrels of oil at Cushing, Oklahoma.

Non-Deliverable

Non-deliverable contracts typically calculate the gain/loss on the contract and the loser pays the winner the net difference.

Example: if you are long an S&P 500 future (ES) and hold it to maturity, you don’t receive or deliver all 500 stocks. You swap the cash value of the contract.

Listed

Listed contracts are traded on exchange and are standardized (same maturity date, same contract size, etc.).

Over the Counter

OTC trades are made with a specific counterparty. In practice, there will be some elements that are standardized (for efficiency), but there is more flexibility (for instance date and size of contract). OTC contracts have counterparty risk (i.e., the counterparty goes bankrupt and doesn’t pay you).

Note: most contracts can be traded OTC or on exchange. Below is what I have typically seen.

Delta One

Delta is the sensitivity of the derivative’s price to the underlying security’s prices (think of slope from school).

Delta One products are those that have a fixed one-to-one ratio. If the underlying moves up or down, the derivative moves up or down roughly the same.

Variable Delta

Options are variable delta, which means the amount their price moves relative to the underlying security changes through time based on certain conditions (examples include time to maturity and distance to strike price).

Common Use Cases

Why would you use derivatives?

Leverage

Capital Efficiency

Rebalancing

Risk management

Part 2 goes into more detail about how you might use derivatives in your portfolio.

Swaps

Definition: Agreement to swap cash flows

Mechanics: Enter into a swap contract with a counterparty and agree to swap cash flows at a certain frequency for a certain length of time. There is always a long and a short position with a swap

Classification: OTC, deliverable and non-deliverable, delta one

Common Types:

Total Return Swaps - one leg will usually be an underlying index with the other being a financing leg

Currency Swaps - agree to swap currencies at particular intervals at an agreed upon exchange rate

Interest Rate Swaps - common is a float for fixed

Pros/Cons:

Pros: You don’t have to roll

Cons: Swaps are rigid. If you want to adjust the size or reverse the position, you will often have to negotiate with your counterparty and redraw up the contract (painful)

Typical Use Cases:

Swaps are good for “core,” predictable positions.

If I know I will have between $1B and $5B in MSCI ACWI (All Country World Index), I can put on a $1B Total Return Swap and then use another more flexible instrument (like a future) to move my position up and down

A corporation knows it will have at least $1B of Euros that it needs every month. A currency swap can lock in the exchange rate and create regular, known flows

A corporation issues floating rate debt but wants fixed. Rather than issue new debt and buy back all the current debt (expensive/time consuming), they can enter into a float for fixed interest rate swap

Forwards

Definition: Agreement to buy (sell) an underlying security at a future date

Mechanics: see definition

Classification: OTC, deliverable and non-deliverable, delta one

Common Types:

Foreign Exchange (FX) Forwards – agree to receive a currency and deliver another on a specific date at a specific exchange rate

Pros/Cons:

Pros: Flexibility to customize

Cons: Counterparty risk, Maintenance (roll/margin)

Typical Use Cases:

Hedging cross-currency transactions

Hedging portfolio currency risk

Speculation on changes in currency

Futures

Definition: Similar to a forward but more standardized and listed

Mechanics: Purchase (or short) a future through an exchange, as the underlying moves

Classification: Listed, deliverable and non-deliverable, delta one

Common Types:

Futures are standardized, so a future is a future. There are nuances between futures based on underlying, but they are beyond the scope of this post

Pros/Cons:

Pros: Exchange traded (near 0 counterparty risk), standardized

Cons: Maintenance (roll/margin), P/L could be exposed to currency risk, Could be costly financing, contract values are large (can be hard to hit specific notional values)

Typical Use Cases:

Rebalancing - If I am redeeming from a manager, they sell the securities and transfer the cash. It takes 5 days to transfer the cash, so I buy a futures contract to maintain exposure

Risk Management - I run a Equity Market Neutral Strategy (which try to have zero sensitivity to the market). After building my portfolio, my residual net exposure is 20%, so I short futures to bring that net exposure to 0%

Hedging - I produce oil and know I will have a certain amount of barrels of oil to sell in August. I short an August oil contract, which locks in the sales price of oil

Credit Default Swaps (CDS)

Definition: Insurance against bond defaults

Mechanics: Buyer of CDS pays a periodic fee to the seller (called the spread). The seller will pay the buyer in the event the bond defaults. Works similar to home insurance or selling a piece of a bonds yield to hedge out default risk.

Classification: OTC/Listed, deliverable and non-deliverable, delta one

Common Types:

CDS is for a specific bond

CDX is for a basket of bonds

Pros/Cons:

Pros: Very specific, clean exposure to credit risk

Cons: Maintenance (roll/margin), painful to trade

Typical Use Cases:

Credit Exposure - I run a Risk Parity portfolio, and rather than trading corporate bonds, which have interest rate and credit risk, I sell CDX to cleanly capture credit risk

Risk Management - I run a bond book that includes corporate bonds. I buy CDS to hedge out some of that risk

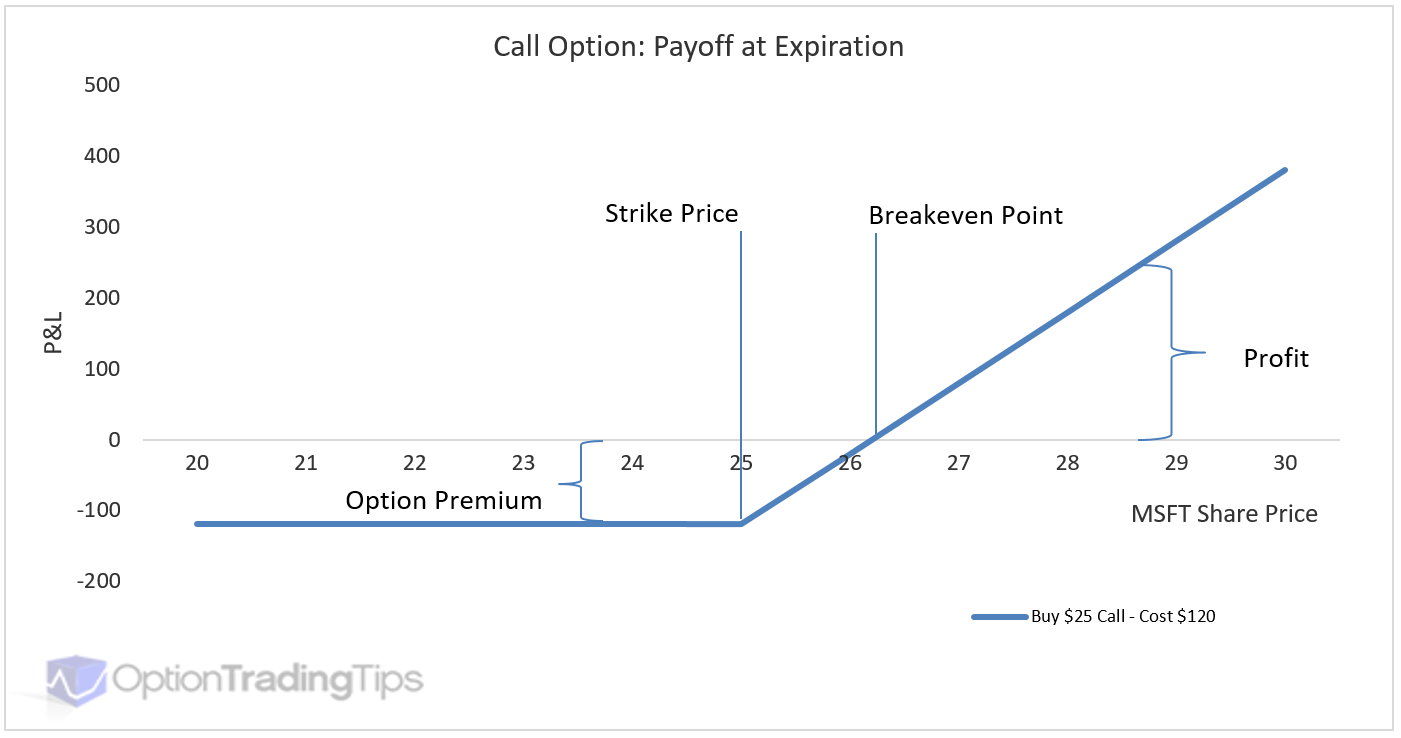

Options

Definition: The buyer has the option (but not obligation) to buy or sell the underlying security for a certain price on a certain day (or before a date for certain options)

Mechanics: The purchaser and seller agree on a date and price (called the strike price) for a certain security, and the purchaser pays an upfront premium for the option to execute or not. If profitable, the purchaser executes the trade. Either way the seller keeps the premium.

Classification: Listed and OTC, deliverable and non-deliverable, variable delta

Common Types:

Options can get exotic, but they all are more complicated versions of the 2 basic structures:

Calls - Option buyer has the option to buy a security at the strike price, and makes money if the underlying securities goes up in price (and they can purchase it for a lower price)

Puts - Option buyer has the option to sell a security at the strike price, and makes money if the underlying securities goes down in price (and they can sell it for a higher price)

Pros/Cons:

Pros: Can be a great risk mitigation tool

Cons: Complicated and you can lose everything

Typical Use Cases:

Rebalancing - If I know I am selling a security in the future, I can sell a call and collect the premium. If the stock goes up, I sell the security (which I would have done anyways), of if it does down, the premium helps offset the loss when I sell it.

Risk Management - I run a trend following strategy and know my payoff profile makes money when trends are strong (either direction) and struggles in flat environments. I can sell option spreads to help in those time periods by selling some of my tails.

Part 2 will go into more detail about how you might use derivatives in your portfolio.